Why China Has No Inheritance Tax

Unpacking the Cultural and Economic Logic as History's Largest Wealth Transfer Gets Underway

Right now, history’s largest generational wealth transfer is quietly underway in China. According to The Economist, over the next decade, Chinese citizens with fortunes above $5 million are expected to pass down roughly $2.1 trillion to the next generation.1

The tax bill for this monumental transfer? Exactly zero.

Across much of the developed world, the inheritance tax is designed for an overarching purpose: to prevent the concentration of wealth and break up permanent financial dynasties. In the United States and the United Kingdom, the estate tax can reach 40%. In Japan, it scales up to a staggering 55%, and in South Korea, structural premiums can push the effective rate even higher.

It is tempting to dismiss this absence as an administrative lag, an assumption that a developing tax code simply hasn’t caught up with the nation’s explosion of private wealth over the last four decades. But a complex and inevitable result driven by three forces:

Cultural DNA: A worldview that treats wealth as lineage continuity rather than individual property.

Historical Mechanisms: Centuries of state-mandated laws that systematically shredded wealth.

Modern Economics: The gravitational pull of capital mobility in Asia and a massive real estate deleveraging.

“Lineage Wealth” vs. “Individual Wealth”

The philosophical foundation of inheritance and estate taxation in the West rests on interpretations of property rights. In the Anglo-American tradition, particularly in the United States and United Kingdom, wealth is closely tied to the individual who accumulated it, and death marks a decisive accounting moment: the individual’s legal and economic identity dissolves, the estate is assessed as a taxable unit, and only then is the remainder transferred to heirs.

Yet this “closing of the ledger” is not merely a liquidation event. It is a point at which competing claims are reconciled, between individual ownership, familial expectation, and the state’s interest in limiting inherited advantage. In this sense, inheritance taxation is less about the state taking a final cut than about redefining the terms under which private wealth can persist beyond the life of its creator.

In the traditional Chinese worldview, however, wealth is conceptualized quite differently. It is a river flowing through a lineage.

When a Chinese patriarch passes his wealth to his children, it is not viewed culturally or psychologically as a “transfer of ownership.” Rather, it is seen as a continuation of the same entity. It is money moving from the left pocket of the family to the right pocket of the family. The very idea that the state would intervene internal family transition to extract a toll feels culturally discordant.

But this cultural preference for keeping wealth within the family creates a historical question: If ancient China didn’t have an estate tax, how did it prevent the rise of entrenched, ultra-wealthy aristocracies that plagued Europe?

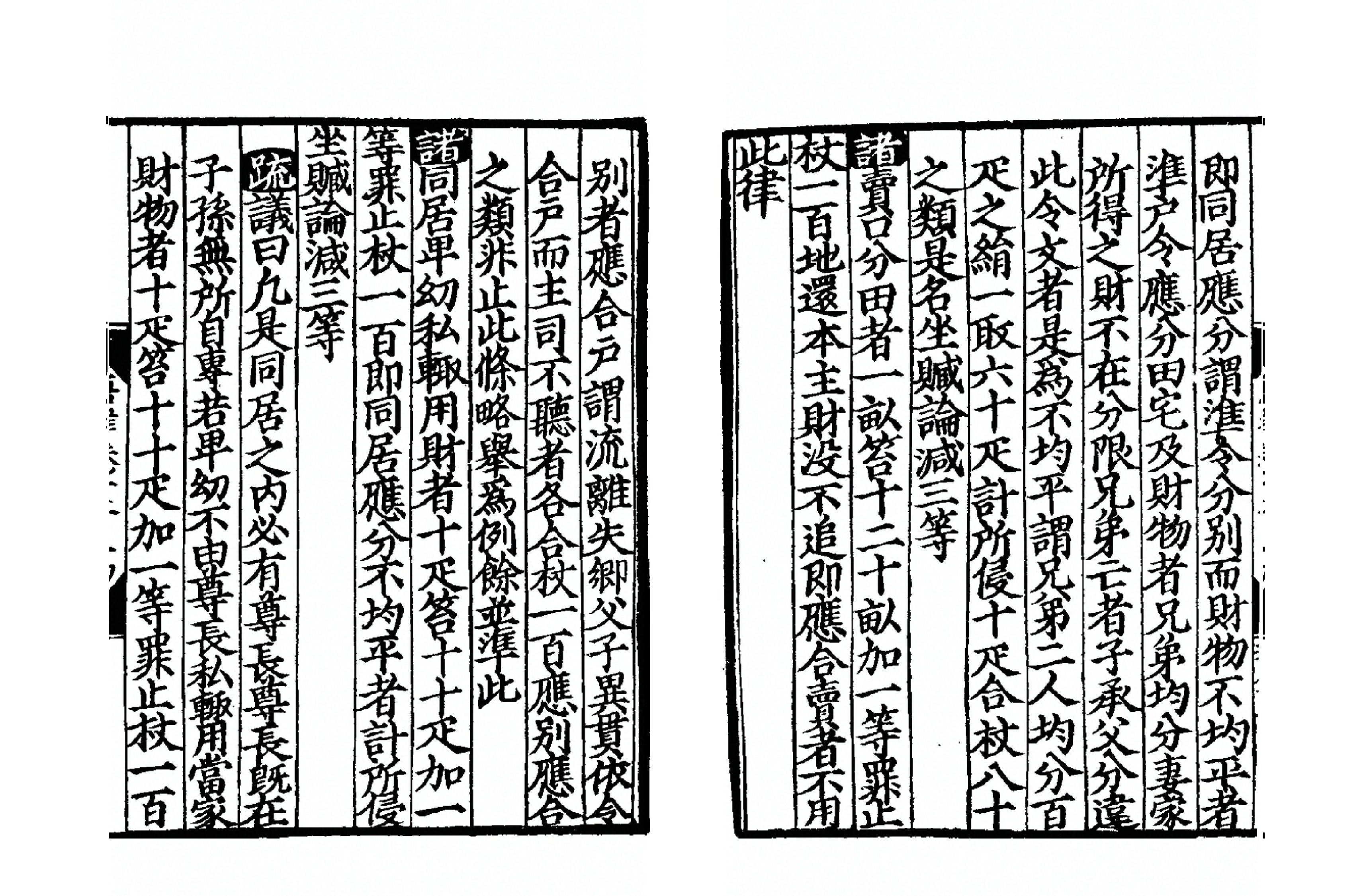

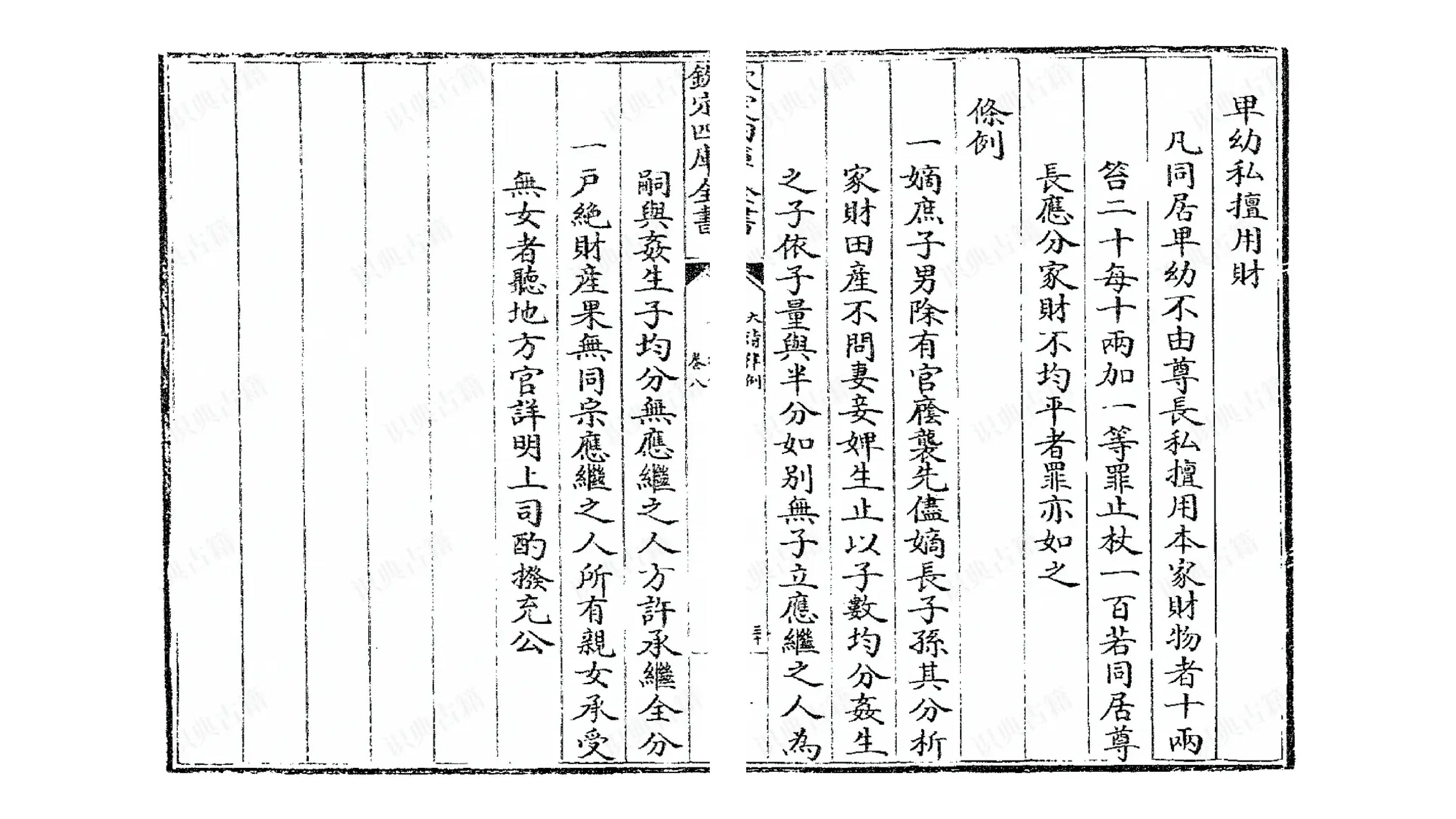

The answer lies in a legal tradition known as Zhuzi Junfen Zhi (诸子均分制), Partible Inheritance.

In the West, the consolidation of wealth was largely driven by Primogeniture, a system where the eldest son inherited the entirety of the estate and the title. This kept massive tracts of land intact for centuries, creating a landed nobility so powerful that modern European states eventually had to invent the estate tax just to break up their monopolies.

Imperial China, codified strictly in the Tang, Ming, and Qing dynasties, mandated the exact opposite. By law, a father’s estate, primarily land, had to be divided equally among all his sons. The concept of “testamentary freedom”, the right to leave your wealth to whomever you choose, did not exist.

If a wealthy patriarch favored his eldest son and wrote a secret will leaving him the entire estate while disinheriting the younger brothers, that document was legally worthless. Upon the father’s death, if the younger brothers took that will to the local magistrate’s office (the Yamen), the magistrate wouldn’t even need to launch a complex investigation. He would instantly void the will and order a mandatory equal division of the assets.

Furthermore, the father’s attempt to hoard wealth for one son would hit a second, equally formidable wall: the Clan. The division of a family estate was a highly public, formalized ritual. It required the presence of clan elders, uncles, and designated witnesses who oversaw the drafting of the division contract. If a patriarch or a greedy son tried to subvert the equal division, the clan leaders had the authority to forcefully intervene to maintain social harmony within the lineage.

Zhuzi Junfen Zhi acted as an automatic, generational wealth shredder. The famous Chinese proverb, “Wealth does not survive three generations” (富不过三代), was not merely a cynical observation about lazy grandchildren; it was a mathematical certainty engineered by the state. Because the traditional family structure dismantled massive estates naturally, the imperial government never needed to develop the administrative muscle of a formal “estate tax.”

When wealth did manage to hyper-concentrate in the hands of a few mega-merchants, like the legendary Shen Wansan 沈万三 of the Ming Dynasty or Hu Xueyan 胡雪岩 of the Qing. The state did not wait for them to die to collect a polite percentage. Imperial power relied on Chaojia (抄家), the total political confiscation of a family’s assets. In the face of absolute imperial authority, the state didn’t need a tax code to redistribute wealth; it simply took it.

Real Estate, Illiquidity, and Economic Timing

While ancient traditions explain the psychological resistance to an estate tax, China's modern economic realities make implementing one practically impossible.